Financialization, not demographics, caused the cost of housing to explode

Written by: Niko Block

February 3, 2026

Solving the housing crisis has been a central plank of the Liberal party during their decade in power, but progress has been elusive. Despite recognition of housing as a “fundamental human right” and pledges of tens of billions of dollars to housing programs, homelessness has risen and affordability has worsened.

Solving the housing crisis has been a central plank of the Liberal party during their decade in power, but progress has been elusive. Despite recognition of housing as a “fundamental human right” and pledges of tens of billions of dollars to housing programs, homelessness has risen and affordability has worsened.

Rising property values have impacted every corner of the market. As home prices have surged, the rate of homeownership has declined across the country, while buyers remain in debt for longer periods of time. Tenants pay higher rental costs, and building social housing is more difficult because of the cost of land.

Policymakers and economists blame high housing prices for a severe supply shortage. This line of thinking led the Canada Mortgage and Housing Corporation (CMHC) to call to double the rate of construction, to build 4.3 million new homes by 2035.

The CMHC’s proposal would increase Canada’s housing stock by 25 per cent over a decade, even though they anticipate population growth of only eight per cent, leading to “abnormally high levels of unoccupied housing units,” as the Parliamentary Budget Office observed. The CMHC’s projected payoff is surprisingly modest: they anticipate real housing prices would only decline to pre-pandemic levels.

These issues point toward a more fundamental question: What is the evidence that a supply shortage has created the housing crisis to begin with?

The trajectory of price, supply and household debt

The “supply-shortage argument” is encapsulated by the CMHC’s claim that “increasing housing supply is the key to restoring affordability.” If the argument is correct, then we should expect to see evidence that increases in dwellings per capita lower prices over time. But historical data show the opposite.

Over the past half-century, dwellings per capita have risen significantly, yet price has risen too, along with household debt. With the exception of home prices, all of the data reported below are from the federal government. The technical version of this article presents the analysis in greater detail, with a methodological appendix as well as footnotes.

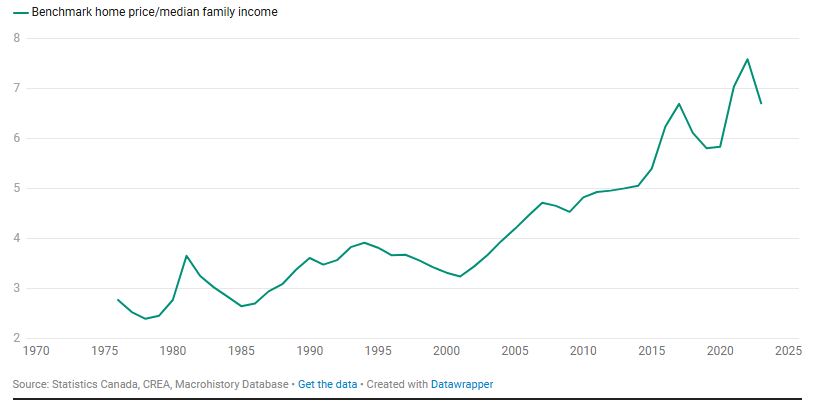

Figure 1. Real home price

In 1976, a standard single-family home in Canada was worth less than three years of income for a two-income household. By 2023, that number had increased to nearly seven years.

In 1976, a standard single-family home in Canada was worth less than three years of income for a two-income household. By 2023, that number had increased to nearly seven years.

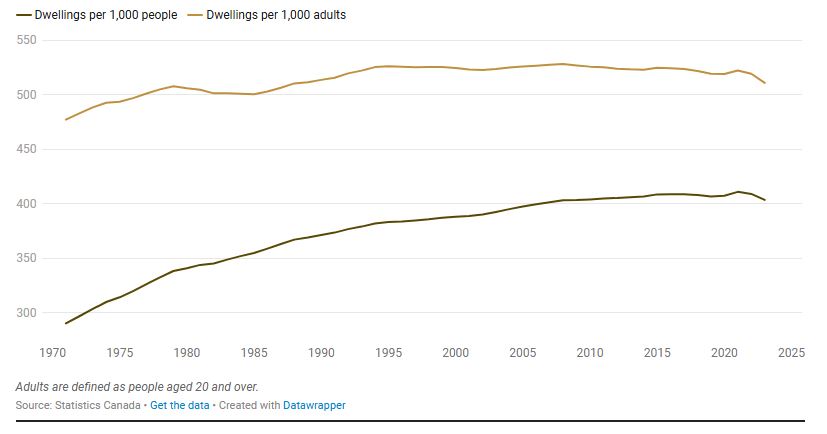

Figure 2. Relative housing stock

The stock of dwellings per capita has risen considerably over that time, from about 290 per thousand people in 1971 to 403 in 2023. Even housing stock relative to the adult population alone (which has remained at a flatter and higher level due to the declining share of children in Canada’s population) has grown, from 477 dwellings per thousand adults in 1971 to 510 in 2023.

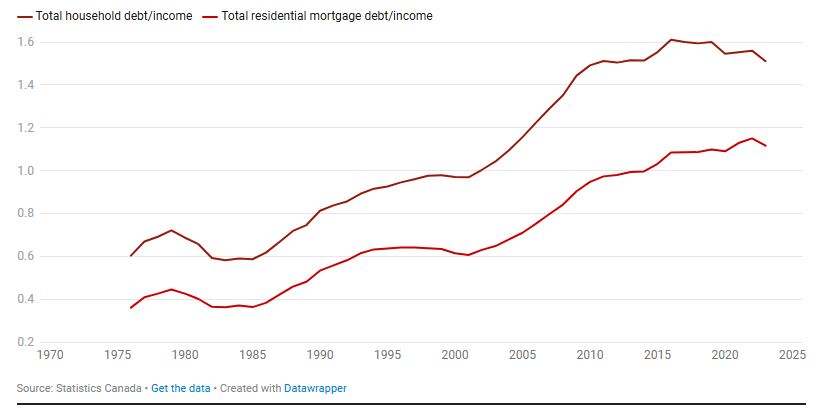

Figure 3. Real household debt

Figure 3 shows the household sector’s mortgage debt and total debt relative to income. Whereas total debt was 60 percent of its annual income in 1976, by 2023 it was 151 percent. Mortgage debt has consistently accounted for two thirds of all liabilities. There are also some clear (if imperfect) parallels between real prices and real debt, with both dipping in 1985 and 2001.

Figure 3 shows the household sector’s mortgage debt and total debt relative to income. Whereas total debt was 60 percent of its annual income in 1976, by 2023 it was 151 percent. Mortgage debt has consistently accounted for two thirds of all liabilities. There are also some clear (if imperfect) parallels between real prices and real debt, with both dipping in 1985 and 2001.

What is the basis of the supply-shortage argument?

In the face of these indicators, it is not viable to argue that a supply shortage has driven housing prices up. There is no shortage of supply. While real prices have more than doubled, housing stock per capita has increased by 39 per cent, and real mortgage debt has more than tripled.

If prices have moved in the opposite direction from what the supply-shortage argument predicts, then how do analysts defend that argument?

First, a small number of studies find that a boost in supply can lead to price reductions. However, there are strikingly few of these analyses and the impact they identify is small. One frequently cited study of New York City finds that a 10 per cent increase in the supply of condominiums reduces condo prices by approximately one per cent within a 500-foot radius.

This finding attempts to isolate the impact of the other factors that can influence housing prices, like interest rates, property taxes, subsidies, and so on. Therefore New York’s condo prices do not necessarily decline when new supply is added; they might just increase less than they would have otherwise, in which case relative supply cannot be viewed as the dominant factor in price determination.

No parallel analysis has been conducted for Canada. The CMHC’s model is the closest thing we have, but they do not make an explicit claim about the extent to which Canadians can expect real prices to decline if, say, we were to boost supply by 10 per cent. Still, the weakness of the evident effect is apparently what has led them to call for a rate of construction well in excess of population growth.

It is difficult to find clear evidence that increased supply pushes price down, because in private markets, new supply only emerges when prices rise and developers feel reassured they can earn a profit on their investment. Price and supply both move up together over time, with increased supply not necessarily pushing prices down.

The second reason for the supply argument’s staying power is that analysts can cherry-pick their evidence by selecting narrow indicators on population or time period. To take one example, Jean-François Perrault highlights the decline in dwellings per capita from 2016 to 2020 and suggests that this was the reason for the sudden price spike during the pandemic. In fact that decline was extremely minor and the 2016 ratio was surpassed by the end of 2021. More importantly, he overlooks the larger picture: that over the long run, dwellings per capita have grown, and yet they are also more expensive.

Some analysts prefer to take households as the key demographic unit, but this approach also reveals no clear evidence for the supply-shortage argument. Census data show that there have consistently been more dwellings than households since 1971. In the intense period of housing inflation since 2001, that ratio has actually risen slightly, from 1,011 dwellings per thousand households to 1,017 in 2021.

On top of that, the square footage of housing units in Canada has on average been growing across all housing types, which should in theory provide more flexibility for people to live with roommates.

No matter how we count population, therefore, the national picture shows no indication that housing inflation has resulted from a concrete shortage of supply.

Although economists have argued fervently that housing supply reduces price, they have been hard pressed to find empirical evidence for it. They do not hesitate to use clear historical indicators to demonstrate that supply responds positively to price increases. But when setting out to demonstrate supply’s downward impact on price, they instead use abstract models that presume what they are trying to explain.

Then what does explain housing inflation?

If a supply shortage cannot explain housing inflation, then what can?

One key counterargument centres the financialization of housing. Describing this phenomenon, the United Nations writes that “housing and real estate markets worldwide have been transformed by global capital markets and financial excess.”

In this view, the housing crisis has been created by banking practices that have directed excessive amounts of credit into the property market, and especially residential mortgages. As a result, buyers can bid prices up to ever-higher levels, resulting in a market where people must pay more for the same type of housing. Hence financialization can be defined as an inflationary tendency in the housing market that is induced jointly by banks’ desire to expand mortgage lending and buyers’ confidence that the value of their properties will rise.

These inflationary pressures are therefore the same as historical speculative bubbles in gold, stocks, cryptocurrencies, or tulip bulbs. Consider, for instance, that record high gold prices today are incentivizing massive extraction projects around the world—and even as the supply of gold has grown, price has continued to rise as well. If and when the price of gold drops, it likely will not be because of the new supply but because of a drop in investor faith.

However, the image of a bubble bursting and prices returning to a more rational “equilibrium” level does not seem to apply to the housing market. Because housing is a necessity, people are willing to pay high prices for it. Bidding wars can therefore persist even when relative supply grows, so long as credit markets enable them.

Proponents of the financialization perspective point to a matrix of institutional transformations that have pushed credit markets in this direction. These include the rise of a global market in mortgage-backed financial assets, the growing importance of credit scores, the decline of property taxes in many areas, and in some cases banks’ growing preference for issuing mortgage loans.

For some Canadian banks, the risk of mortgage lending has been lowered by complex instruments that insure against losses, the most significant of which are offered by the government itself. Additionally, central banks in Canada and beyond have at times implemented unconventional monetary policies that strongly encourage expanded lending by banks.

The financialization argument may be less straightforward and harder to test than the supply-shortage argument, but what it lacks in elegance it might make up for in accuracy.

A crisis of distribution

The housing crisis is not a crisis of supply; it is a crisis of distribution. Housing inflation has boosted owners’ wealth substantially—a particular windfall for those who own multiple properties and carry little mortgage debt. Meanwhile, rising prices have put homeownership out of reach for many Canadians and put new buyers deeply in debt, while driving up homelessness.

There are two clear implications for policymakers. First, improving affordability may require ambitious regulatory reform in the banking sector. Many analysts have made robust arguments to this effect, which deserve to be taken seriously and explored further.

Second, there is no evidence that demographic pressures have contributed to the steep housing inflation Canada has experienced in recent decades—meaning that policymakers cannot reasonably blame immigration for the long-term trend. Over the past half-century, the number of housing units has risen substantially relative to population, and their average size has increased as well.

In spite of the clear evidence to that effect, the supply-shortage argument has remained dominant among policymakers, journalists, and economists. Regardless of the motives behind that consensus, the effect has been to direct attention away from the material conflict between owners and non-owners within Canada, and towards a fictitious conflict between Canadians and non-Canadians.